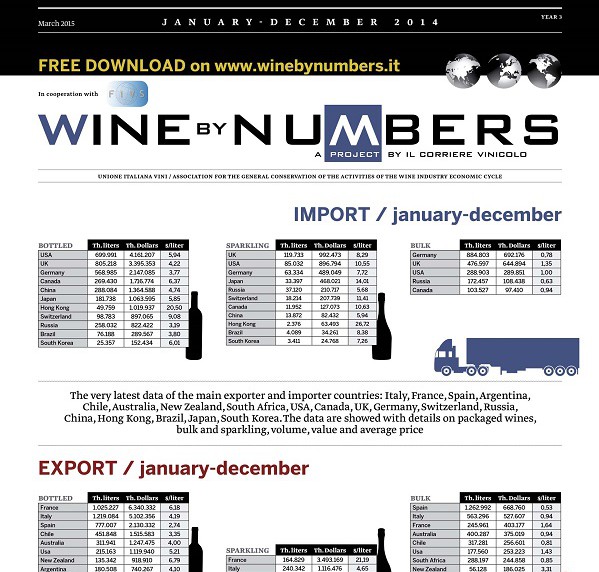

The year began with the intent on growing, but it then became more a question of fending off others. Not always succeeding. None of the major exporting countries ended sales in 2014 without a few black marks. Moreover, the same goes for the Europeans (which still seem to have a little something extra) and for the New World.

In Italy there was extensive growth as regards sparkling wines, thanks to the driving force of Prosecco, while growth was modest, almost nil as regards bottled wine. As for bulk wine, the Spanish tsunami wiped away the Italian wines from strategic markets such as Germany and Eastern Europe, and made it impossible to apply the needed price increases after a very poor harvest.

Hence, Spain celebrated record exports, albeit with minimum prices, after a monstrous 2013 harvest that drove wineries to sell off their wine to empty stocks. The year was not at all exciting for bottled wine or sparkling wine, though, especially on the large markets such as the UK, Germany and the USA.

France, however, toasted for the return of Champagne, yet cried over the Bordeaux disaster not only in China but also in the West, a disaster that was only partly offset by the good performance recorded by “second liners”, such as Languedoc, Alsace and the Loire. An anonymous year for Burgundy wines.

On the other side of the world, the United States confirmed the state of grace in Canada, but saw low performance on the Eastern markets, partly due to the increase in the dollar at the end of the year.

Argentina and Chile had quite different dynamics: between the two, the Chileans were relatively better off. They lost a few points in Europe and did not fare well in the USA but they were successful on close markets (Brazil first and foremost) and increasingly successful in the East (Japan, China, South Korea), favoured by bilateral agreements that allow great competitiveness to Chilean bottles.

This cannot be said for the Argentines. They struggled with a dramatic internal crisis and continued to lose ground in North America, the most important market for the Andean cellars. Things looked better in Brazil and South America in general, and an interesting window opened in the UK.

Let’s look at Oceania. Here was the return of New Zealand, which seemed to have restored order to its supply, recovering important value in key markets such as the UK and USA, and keeping one foot firmly in the neighbouring Eastern markets. The Australians, however, failed in this and they now have two very distinct roles on the markets: one is for bulk wine, which is mostly popular in the UK and continues to grow (the ratio with bottled wines is now at 80/20). The other role is for bottled wine, whose loss of market share in North America was not compensated in the past year by credible growth in Japan and China, which ended up clouding over even the good market performance in Hong Kong and Singapore. And this despite the lightening of the weight of the Australian dollar over the year.

Finally, South Africa. The country experienced a rather neutral 2014, although it did find a slight readjustment in the bulk/bottled wine ratio in favour of the latter. The readjustment was due not so much to the resounding growth of bottled wines as much as the reduction in sales of bulk wines, which were replaced everywhere by the cheaper Spanish products. At this time in 2013, it was South Africa that played the role of Spain today.

All the data and figures on Wine by Numbers Quarterly Edition, freed download here